OPEN UNIVERSITY MALAYSIA

FACULTY OF BUSINESS MANAGEMENT

BBMR 4103

RELATIONSHIP MARKETING

Name: Adam Khaleel

Lecturer: Hussain Sunny Umar

Learning Centre: Villa College

Trimester: May 2013

Contents

1.0 Executive Summary

The assignment will mainly talk about the relationship marketing strategies adopted in Bank of Maldives and the recommendations to improve its relationship marketing strategies in future.The first part of this assignment will give an introduction of BML covering the nature of the company, vision, mission, core values, market size, market position, products and services, target market and the competitors.The second part will give an analysis of existing customer relationship strategies covering the good customer relationship strategies adopted and some challenges faced to build a good customer relation with its customers.The fourth part will talk about the recommendations to enhance and improve their existing customer relationship strategies and to overcome the challenges faced by them. Finally, a conclusion of this assignment will be given.

2.0 Introduction

Today’s business environment is very competitive compared to earlier. The customer expectation is increasing due to this high competition among the businesses. Most of the businesses are engaging in marketing activities but are fewer firms are concern with the relationship marketing. Most of the firms are trying to increase sales rather than building a good relation with their customer. Although this is the case, relationship marketing is crucial for all the businesses such as Bank of Maldives to retain the customers as well as to get more customers in future.

Customer relationship management is a broad strategy and process of acquiring, retaining and connecting with particular customer to create higher value for company and the customer (Parvatiyar and Sheth, 2001). According to Vavra (1992) relationship marketing is retaining the customers by using variety of after marketing strategies that lead to customer staying in touch after the sale are made.

Bank of Maldives was registered as a company on 23rd May 1982 and it was listed on 10th November 1982. After the registration they were given the license to provide banking services in Maldives. Bank of Maldives Plc. was inaugurated on 11th November 1982 and started business process as a joint venture bank with 60% of shares by the Government of the Maldives and 40% shares owned by IFIC Bank Ltd from Bangladesh. Maldives government decided to restructure the BML and purchased the 40% shares held by IFIC Bank Ltd. The Government decided to sell BML shares in December 1992 to the public in order to develop the Bank’s capital. Today, the BML has 26 branches in Maldives of which three are in Male and the rest are in different atolls (BML, 2010).

The banking industry in the Maldives includes seven banks which are 2 locally incorporated banks, 4 branches of foreign banks and a subsidiary of a foreign bank. The competitors for BML include Bank of Ceylon, State Bank of India, Mauritius Commercial Bank, HSBC, Habeeb Bank and Maldives Islamic bank. The balance sheet shows the assets value of the bank has been increasing over the past three years. It has liquid assets around 31% of its assets. It has around 40% of market share. As of Dec 31, 2010, tourism, construction and fishing industries accounted for 80% of the BML’s loan exposures with the share of tourism standing at around 60% (Credit Analysis & Research Limited, 2011). The net profit of the BML for 2012 has reached over MVR 200 million. Hence, BML has high market share and high market growth (“BML net profit”, 2012).

Currently, the BML is providing the services like various bank accounts, card services, transnational travel and payments, internet banking, bill pays, personal loans, prepaid recharge, mobile banking, ATM services, direct debit, business card solutions, loan and leasing and merchant service solutions. The target market is the whole population of Maldives including the foreigners in Maldives. The potential customers include businesses, the individuals in Maldives and Maldivians in international countries (students and businessmen who use bank facilities) (BML, 2010).

The vision is to lead the way through quality of service and dedication of their staff. The missions include becoming the leader in the financial industry in Maldives by spreading its presence in all key economic geographies in Maldives and promoting long term saving culture in the nation. The values are integrity, innovation, respect, communication and service (BML, 2010).

3.0 Analysis of existing customer relationship strategies

Bank of Maldives is concentrating on a new business model which is mainly focus on the creation of good customer relation. The following part will show how far the relationship models are adopted in BML.

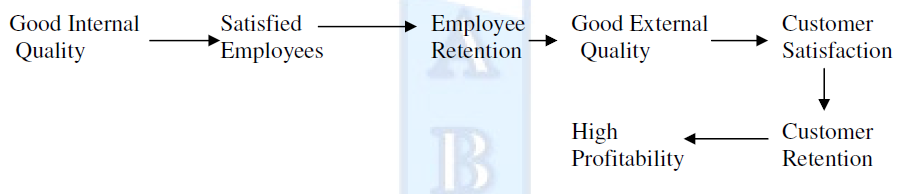

3.1 Relationship model

The relationship model by Gummesson (1999) says that good relationships will leads to good external quality and good customer satisfaction. When there is good quality in internal relationships, the employee relationships will be improved. When the employee relation improves the external quality and customer satisfaction will be improved. As a result of this customers can be retained and profit of the firm will increase.

3.2 Existing good CRM strategies

1. Automatic Renewal of Debit Cards

BML is trying to improve customer satisfaction by introducing an automatic renewal process for American Express and Visa Debit Cards. The customers are no need to visit the card center to get a new debit card and the debit cards can be renewed before the expiry date of the cards. The purpose of this process is to help customers to get good banking services (BML, 2013).

2. Third-party Encashment

BML has decided to change the system for withdrawals maximum to RF 25000 and $1500. This change will help to avoid probable losses that may arise from third-party withdrawals from the customers’ accounts (BML, 2013).

3. Financial Awareness Program

BML has held different financial awareness programs between the youth. BML conducted this program in March 2013 at Ghiyaasuddin School to give information about banking and the banking products and services provided by BML. BML conducted an awareness program for general public about Islamic Banking and Finance which was aired by MBC in March 2013 and broadcasted by Voice of Maldives because they are going to introduce Islamic Banking soon (BML, 2013).

4. Human Resource Development

BML has different learning and development programs for their staff. In the beginning of 2013, they have started training sessions on basics of Islamic Banking, Microsoft excel training and professional English training. Besides, some employees were given the chances to join the external trainings such as Fraud and Forensic Accounting Training which were held in Maldives and in abroad (BML, 2013).

BML has performance management processes for the staffs at end of each year. They had 818 staff as at March 31st 2013 and they have recruited 20 staff in the first quarter of 2013. They also have manager’s refreshing Programs on human resource related issues (BML, 2013).

5. Redefining the Branch Concept

BML has introduced a new banking service for the customer in order to enhance the customers’ experience. BML Lite provides more customer friendly services which assists easy and quick access to the services. This is the first branch which provides banking services six days in a week. The customers can deposit Rufiyaa, US Dollar and cheques 24 hours a day through the deposit machines in this branch (BML, 2012).

6. Facilitating E-Banking

BML is trying to improve internet banking service. They internet banking transactions limits were increased and ATM withdrawal limits were also increased. BML introduced a free internet banking premium package on 1st January 2013 in order to improve customer experience (BML, 2012).

7. Integrating Customer Satisfaction with Performance Management

BML conducted 3 customer satisfaction surveys in 2012 in order to restructure BML towards a more customer oriented company. The research helped them to assess the customers’ satisfaction levels, identify the gaps in customer service and to measure the brand loyalty of the customers. After the surveys, all branches are focus on customer satisfaction. BML introduced service excellence awards to improve the service and to encourage competition between branches (BML, 2012).

8. Leveraging Social Media

In order to demonstrate its promises and to be transparent, they have introduced Facebook page and Twitter account. BML is using these channels to get customer feedback and as a customer service platform (BML, 2012).

9. Helping Community Growth

BML is focusing on CSR for their success. They distributing pension by their Dhoni Banking in order to provide access to their services to the whole population in Maldives. Their CSR activities in 2012 were mainly focused on community well-being, education of the students, developments of the Nation and youth. They have opened a computer lab in Addu City, Hithadhoo School in 2012. They have provided funds for local NGO computer laboratory in order to prevent the issues of abuse of illegal drugs in the country (BML, 2012).

BML is participating and funding to the social and community activities in the country. In 2012, they provided a HD projector and a project screen to Youth Centre in Male’. BML is one of the main sponsors of the Fisherman’s Day celebrations and for the 2012 National Quran Competition. BML is providing funds to Islamic Affairs for developing and maintaining of mosques in Maldives. They participated in Youth Challenge 2012 and sponsored recent Independence Day celebrations. They also have sponsored the local Twitter community’s futsal tournament (BML, 2012).

10. Serving the Unbanked Population

BML has expanded their services to inaccessible rural areas in the country by visiting these areas. In 2012, they have made over 2000 trips to provide their services and to provide pension allowances to the pension holders in various islands (BML, 2012).

11. Customized Financial Solutions for Corporate Customers

BML has supported the business community by offering a wide range of corporate and commercial banking products and services. They helped the resort sector by providing working capital and new development funding. They are supporting the construction industry by providing construction loans (BML, 2012).

12. Encouraging the Risk Management Culture

In 2012, BML developed complete Risk Management approach to their company. Besides Credit Risk Management, their Central Risk function helps for all the recovery works, operational risk, liquidity risk and regulatory compliance (BML, 2012).

13. They have long-term strategies

According to their vision statement, they are focusing mainly to provide quality service by empowering their staff. It also says that they always listen to their customer needs and are trying to increase customer confidence and satisfaction level. This is a very good strategy because the customer relationship must be always long-term to retain their customers in future (BML, 2012).

The strategies adopted by BML are related to the above relationship model. The human resource development strategy is linked to the very first stage of the model and the other strategies are linked to the customer satisfaction stage. Therefore, these strategies are linked with each other in as shown in the relationship model diagram. However, there are some challenges to their customer relationship management.

3.3 The Challenges

1. ATM Issues

The first issue with the ATMs is BML does not have enough ATMs in various parts of Maldives. Although they are having one branch in each atoll, they do have enough ATMs in these atolls. As a result of this many of its customers are unable to withdraw money in their atolls and they have to travel to another atoll or island to withdraw money. Male’ is the capital of Maldives and more than one third of the population is living in Male’ but BML is unable to provide good ATM service to the customers especially when the people get their salary. Customers have to spend more time in the queues to withdraw money. At the end of each month when the salary is deposited to the customers’ accounts, most of the ATMs are out of service due to high withdrawal (A. Hamza, Personal Interview, May 14, 2013).

The issues with the ATMs are sometimes customers do not get the cash or receipt after the accounts are being debited. The receipts after the transactions by ATM are very important for the customers because if the customers want to claim for compensation it will be very easy to trace the problem (A. Hamza, Personal Interview, May 14, 2013).

2. Bank queues issues

BML’s customers have long queues to buy dollar and for the other transactions. The customers are getting less token numbers for dollar purchase. The customers’ have to wait long time in to get service from the bank because more customers are getting their service from the BML. As a result of this many customers are dissatisfied with the BML’s service (“Merchants voice”, 2011).

3. Customer care issues

Sometimes the customers are unhappy about the customer service provided by BML. When a customer calls to report an issue, the customer does not get answers. Some customers complain that the staffs do not answer their queries even during the working hours (“BML to add”, 2012).

4. Customer secret information issues

There was news about the government raid into BML and took away some files of secret information about the customers. As a result of this some customers switched to other banks like HSBC, SBI, and Bank of Ceylon (“No Confidence”, 2011). There was also a news about the BML will be giving some details about customers banking history and other information to third parties. As a result of this the confidence on BML has decreased (“How Safe”, 2011).

5. Fraud Issues

There are fraud cases by BML’s employees from customers’ bank accounts in the recent years. It has been reported that an employee works in the BML’s Gaafu Dhaalu atoll Villingili branch has been suspended for an unauthorized transfer of MRF 2000 from a customer's account to another account. This has lost some customers trust on BML (“BML suspends”, 2011).

6. Online Security issues

Recently BML has advised its customers not to send their personal details like bank card numbers, account numbers through emails after giving a warning about the fake e-mails being sent in the BML’s name (“BML issues”, 2013).

4.0 Recommendations to improve customer relationship strategies

Although, BML has some challenges to their customer relationship management, they can overcome these challenges and can improve the existing customer relationship strategies by adopting the following recommended strategies.

4.1 Improve ATMs

ATMs are very essential for BML to build a good relation with its customer. BML has to improve their ATMs by increasing their branch networks and installing ATMs in strategic locations where more people can reach. They need to install more ATM’s in locations where existing ATM’s are located in order to cater the high demand during the end of each month (Pokharel, 2011).

It is also important to place instructions near ATMs to explain the use and a demo by showing which transactions can be done by ATMs and the ATM transactions procedures. Hence the customers will feel more confident when they use ATM’s. It is also very important provide an easy way to get compensation for the customers who do not get cash due to possible errors in ATM transactions (Pokharel, 2011).

4.2 Use a Queue Management system

It is recommended to use a queue management system in BML. This system is powered by the cell phones. This will help to manage several waiting lines at the same time and can interact with customers by text notices or a digital display. The patient, student and customer are free from standing in lines. They can roam without the anxiety of losing their place in lines. So, BML will be able to get a solution for the queue issues in their company (Nexa Group Pty Ltd, 2013).

4.3 Online security management

It is important to have an effective security management which will help in layering the number of solution that focus on people, processes, technologies and risks. When all these layers are combined, it will create a great tool that can help BML a successful way to overcome its security challenges than a single individual solution. BML always need to aware and engage the customers about the online security (Ashfield & Shroyer, 2009).

4.4 Customer care management

BML need to handle the customers’ complaints in a systematic way. BML need to train the employees to handle dissatisfied customers. They need to employ efficient employees in their call center with required facilities. BML also need to maintain the customers’ personal information confidential in order to avoid losing of their customers (Pokharel, 2011).

4.5 Select the honest and qualified employees

It is very important to hire honest employees for the job because Banks are the organizations which have to safeguard customers’ money. This can be done by recruiting the qualified employee who does not have past fraud records. They should have good interviews to select the right employee for the job. In addition to this, they need to give proper training to the employees and they need to compensate the customers who might lose the money by a dishonest employee (Pokharel, 2011).

4.6 Increase Switching Cost

BML should have strategies which will increase the switching costs of its customers in order to retain their customers and to increase the customers share. The switching cost can be increased by providing excellent services, good customer service, focus on differentiation strategies, having emotional links with customers and making they feel as a valued customer (Pokharel, 2011).

4.7 Build Brand Image

BML need to have extroverted culture to promote its brand name. This change should be followed in all the levels of the company. Employees are the most important people to build a strong brand. BML needs to prepare its employees with the required approaches and skills hence the employees will play as an ambassador role in promoting their brand name (Pokharel, 2011).

5.0 Conclusion

Bank of Maldives is a successful company in banking industry in Maldives. Although there are many competitors in the market, they are covering a high market share. They have their branches throughout the country. They are providing variety of products and services to their target markets.

The analysis of their existing customer relationship strategies shows that they are having various good relationship strategies like focusing on customer retention, orientation of product benefits, long-term concentration, high customer service, high customer commitment and high quality services. These strategies include easy ways to renew the debit cards, third party enhancement, participating in different occasions, providing awareness programs, developing their human capital, redefining branch concept, facilitating e-banking, integrating customer Satisfaction with performance management, having different social media, helping the community growth, assisting various sectors developments, serving the unbanked population , and other countries for the development of the country.

However, there are some challenges to their customer relationship management like issues with ATM’s, their customer queue issues, customer care issues, issues with the maintaining of customers’ confidential information, employee fraud issue and online security issues.

Although, BML has some challenges to their customer relationship management, they can overcome these challenges and can improve the existing customer relationship strategies by improving their ATM services, adopting the cell phone queue management system, strengthening the online security system, providing quality customer care service, selecting the honest employees, increasing the customer switching cost and building a strong brand image of the company.

As a Marketing Manager’s opinion, BML can enhance their existing customer relationship strategies by adopting the recommended strategies to retain its customers and to get more market share in future.

6.0 Reference

Ashfield, J., M. & Shroyer, D. (2009). Security Management: An Ongoing Challenge for Banks. Retrieved May 15, 2013, from http://www.banktech.com/risk-management/security-management-an-ongoing-challenge/214303644

Bank of Maldives issues email scam warning to customers. (2013, April 29). Minivan News. Retrieved May 15, 2013, from http://minivannews.com/news-in-brief/bank-of-maldives-issues-email-scam-warning-to-customers-57147

Bank of Maldives net profit for 2012 rises to MVR 200 million. (2012, October 31). Minivan News. Retrieved May 11, 2013, from http://minivannews.com/news-in-brief/bank-of-maldives-net-profit-for-2012-rises-to-mvr-200-million-46488

Bank of Maldives to add 19 new ATMs. (2012, November 03). Minivan News. Retrieved May 14, 2013, from http://minivannews.com/news-in-brief/bank-of-maldives-to-add-19-new-atms-46631

Bank of Maldives. (2012). 2012 Annual Report. Retrieved May 12, 2013, from http://www.bankofmaldives.com.mv/SiteCollectionDocuments/BML%20-%20Annual%20Report%202012%20-%20English%20-%2009%20May%202013%20%28small%20file%29.pdf

Bank of Maldives. (2013). First Quarter Report, January to March 2013. Retrieved May 12, 2013, from http://www.bankofmaldives.com.mv/SiteCollectionDocuments/1st%20Quater%20Report%202013.pdf

BML suspends employee over Rf2,000 fraud. (2011, August 23). Haveeru online. Retrieved May 15, 2013, from http://www.haveeru.com.mv/fraud/37287

Bank of Maldives. (2010). Company Background. Retrieved May 11, 2013, from http://www.bankofmaldives.com.mv/INVESTORRELATIONS/CB/Pages/default.aspx

Credit Analysis & Research Limited. (2011). Report on Bank of Maldives. Retrieved May 11, 2013, from http://www.careratingsmaldives.com/Files/Bank_of_Maldives_writeup_Final.pdf

How safe is your account in Bank of Maldives. (2011, April 07). Maldives Today Time press. Retrieved May 14, 2013, from http://www.maldivestoday.com/2011/04/07/how-safe-is-your-account-in-bank-of-maldives/

Merchants voice concerns over police operation against dollar black market. (2011, March 29). Haveeru online. Retrieved May 14, 2013, from http://www.haveeru.com.mv/english/details/35066

Bank of Maldives. (2010). Our Commitments. Retrieved May 11, 2013, from http://www.bankofmaldives.com.mv/InvestorRelations/Pages/OurCommitments.aspx

Bank of Maldives. (2010). Personal banking and business banking. Retrieved May 11, 2013, from http://www.bankofmaldives.com.mv/PBanking/Pages/default.aspx and http://www.bankofmaldives.com.mv/BBanking/Pages/default.aspx

Gummesson, E. (1999). Total Relationship Marketing: Rethinking Marketing Management from 4Ps to 30Rs. Oxford: Butterworth Heinemann.

Nexa Group Pty Limited. (2013). Queue Management. Retrieved May 15, 2013, from http://www.nexa.com.au/queue-management/

No Confidence of Banks. (2011, April 10). Maldives Today Time press. Retrieved May 14, 2013, from http://www.maldivestoday.com/2011/04/10/idiots-guide-to-dollar-shortage-in-maldives/

Parvatiyar, Atul and Jagdish N. Sheth (2001), Customer Relationship Management: Emerging Practise, Process, and Displine. Journal of Economic and Social Research, 3(2), 1-34.

Pokharel, B. (2011). Customer Relationship Management: Related Theories, Challenges and Application in Banking Sector. Banking Journal, 1(1). Retrieved May 15, 2013, from http://www.google.mv/url?sa=t&rct=j&q=Customer+Relationship+Management:+Related+Theories%2C+Challenges+and+Application+in+Banking+Sector&source=web&cd=1&cad=rja&ved=0CC0QFjAA&url=http%3A%2F%2Fwww.nepjol.info%2Findex.php%2FBJ%2Farticle%2Fdownload%2F5140%2F4272&ei=zbWXUbHXG8KJrQfLrYCwDA&usg=AFQjCNGw7SpwhDqyaUCLYEQ6NlSS4AoCyw&bvm=bv.46751780,d.bmk

Vavra, Terry G. (1992), After marketing: How to keep customer for life through relationship marketing. Homewood Ill.: Business One Irwin.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.