Open University Malaysia

Faculty of Business Management

BBPW3203

FINANCIAL MANAGEMENT 2

Name: Adam Khaleel

Lecturers: Abdul Munnim and Hassan Waheed

Learning Centre: Villa College

Trimester: September 2012

Contents

Executive Summary

Since the shareholders are the owners of the company, the company’s dividend policy is very important one for its shareholders as well as for other investors. The purpose of this assignment is to analyze and evaluate firm’s dividend policy. The three companies that I have chosen for this assignment are from Bursa Malaysia. In this assignment, firstly, a brief introduction about Mitrajaya Holdings Berhad from capital goods sector, Metal Reclamation Bhd from basic materials sector and AirAsia Bhd from transportation sector which are listed in will be given. Secondly, the different types of dividend policies a company can use in practice will be discussed. Thirdly, the analysis of dividend policies of these companies will be given for the years 2009, 2010 and 2011. Fourthly, a detailed evaluation of dividend policies among these companies will be given. Finally, a justification will be given for the analysis and evaluation of dividend policies of these companies.

INTRODUCTION

Since the shareholders are the owners of the company, the company’s dividend policy is very important one for its shareholders as well as for other investors. The purpose of this assignment is to enhance the ability to analyze and evaluate firm’s dividend policy. The three companies that I have chosen for this assignment are from Bursa Malaysia.

In this assignment, firstly, a brief introduction about Mitrajaya Holdings Berhad from capital goods sector, Metal Reclamation Bhd from basic materials sector and AirAsia Bhd from transportation sector which are listed in will be given. Secondly, the different types of dividend policies a company can use in practice will be discussed. Thirdly, the analysis of dividend policies of these companies will be given for the years 2009, 2010 and 2011. Fourthly, a detailed evaluation of dividend policies among these companies will be given. Finally, a justification will be given for the analysis and evaluation of dividend policies of these companies.

The companies’ backgrounds;

MITRAJAYA HOLDINGS BERHAD (MHB)

Mitrajaya Holdings Berhad was established in 1985. Today, they are operating in capital goods sector and in construction industry in Malaysia. Mitrajaya Holdings Bhd through its principal subsidiary, Pembinaan Mitrajaya Sdn Bhd, has created for itself an enviable track record of successful projects in construction and civil engineering related fields. Mitrajaya has long been a major player in helping Malaysia become a nation with modern infrastructure, as well as providing quality living and working environments. They have played a significant role in major national projects such as the Kuala Lumpur International Airport projects (Mitrajaya: Our business portfolio, 2012).

Their construction division has grown with the great infrastructural transformation in Malaysia that has undergone in a short period of time. This process includes the rapid building of the country's major hubs of transportation, commerce and finance. Meantime, in collaboration with international consultants, the Division has undertaken the completion of hotels, resorts, power plants, highways and golf courses. They are now a multi-national conglomerate with businesses in a diverse range of industries, among them, construction, property development, international projects, manufacturing as well as healthcare (Mitrajaya: Our business portfolio, 2012).

Mitrajaya's mission is to provide timely and quality services to all its customers by exercising due care to the environment, upholding best business ethics, meeting its social obligations, meeting employee expectations and optimizing shareholder value. The vision is to be the preferred product and service provider in all their core businesses (Mitrajaya: Our business portfolio, 2012).

METAL RECLAMATION BERHAD (MRB)

Metal Reclamation Bhd is a public listed company in Malaysia and having its shares listed on the Bursa Malaysia Securities Berhad since 4 June 1998. They are operating in basic materials sector and in metal mining industry in Malaysia. Their principal activity is investment holding while their subsidiaries’ core activities are involved in the business of smelting, recycling, refining and sale of lead and lead alloys. The MRB Group includes MRB and other four subsidiaries (Metal Reclamation Bhd: About us, 2012).

The MRB Group also has since 2004 acquired a 47.5% equity interest in Nutek Pte Ltd, a company incorporated in Singapore and this primary business is manufacturing automated equipment for the electronic and electronic related industries. Its products are marketed internationally with branch offices in North and South America, Europe and across Asia (Metal Reclamation Bhd: About us, 2012).

Their vision and mission are to be the most competitive and largest lead producer in South East Asia, to adopt the most suitable technology in lead production, to achieve the high safety, health and environmental standards, having achieved ISO 9002 they are targeting themselves towards ISO 14001 (Metal Reclamation Bhd: About us, 2012).

AIRASIA BERHAD

AirAsia was established in 1993 and commenced its operations on 18 November 1996. They are operating in transportation sector and in airline industry in Malaysia (AirAsia: Corporate profile, 2012).

They launched their first international flight to Bangkok in 2003 when they opened a second hub at Senai International Airport in Johor Bahru. Later they started a Thai subsidiary by including Singapore to the destination list and started flights to Indonesia. In June 2004 started flights to Macau meanwhile flights to Mainland China and the Philippines started in April 2005. In late 2005 flights are started to Vietnam and Cambodia and in 2006 to Brunei and Myanmar. AirAsia took over Malaysia Airlines's Rural Air Service routes in Sabah and Sarawak, in August 2006. They have enhanced its operation in Asia by connecting all the existing cities in the region and expanding further into Indochina, Indonesia, China and India. AirAsia is expecting to grow further with the increased frequency and addition of new routes (AirAsia: Corporate profile, 2012).

AirAsia’s vision is to be the largest low cost airline in Asia serving the 3 billion people who are currently underserved due to poor connectivity and high fares and it expects to be a the leading low-cost carrier in the Asian region. Their mission is to be the best employer, create a globally recognized ASEAN brand, to be the lowest cost budget airline and to maintain the highest quality service by latest technology (AirAsia: Corporate profile, 2012).

TYPES OF DIVIDEND POLICIES

A dividend is the distribution of a firm’s income to its shareholders. Dividend policy determines what happens to the value of the firm as the dividend increases or decreases, holding everything else constant. It is to retain profits or to distribute dividend to shareholders (Aliahmed, 2011, p. 86-103).

The dividend payment is a fundamental decision that financial managers make because it not only communicates to the market participants but also has signal effects. The value of the stock is the present value of expected future dividend (Aliahmed, 2011, p. 86-103).

Constant Payout Ratio Policy is very rarely used among companies. The dividend payout ratio is calculated by dividing cash dividend per share by earnings per share. This indicates the percentage of ringgit earned for each share that is distributed to shareholders. This policy helps firms to establish a certain percentage of earnings to be paid to owners in each dividend per share. However, if the firm makes loss or earn less, the dividend may be lower or even omitted for a certain period (Aliahmed, 2011, p. 86-103).

Constant Nominal Dividends (Regular Dividends): this type of policy firm maintains a fixed ringgit dividend. This is also called a regular dividend and this is a level that the board of directors hopes to maintain in the future. However, it could be increased or decreased if the earnings increases or decreases. This type of dividend is much important for investors as this gives a constant income to shareholders and reduces uncertainty of dividend in future (Aliahmed, 2011, p. 86-103).

Special Dividends Payout Policy: Firms sometimes issue extra dividend and special dividends to their shareholders on certain occasions. This is done when the earnings are far better than expected in a given period and the firm may pay this additional income as a form of special dividends (Aliahmed, 2011, p. 86-103).

Cash Dividend Payments and Payment Mechanisms: The cash dividend is paid on the payment date to all shareholders of record on the record date. To be a shareholder of record, and thus receive a dividend, one must have purchased the stock before the ex-dividend date. Instead of cash dividends, many companies have automatic reinvestment plans in which additional shares of stock are purchased (Aliahmed, 2011, p. 86-103).

Chronology of Dates of Dividend Payment;

Declaration date: Firm’s board of directors meets to declare future dividend payments on a certain date and the dividend will only be payable to shareholders of record (Aliahmed, 2011, p. 86-103).

Ex-dividend date: Investors buying the stock before this date are entitled to the dividend declared. Shareholders purchase shares on or after the ex-dividend date are not entitled to the dividend (Aliahmed, 2011, p. 86-103).

Record date: Those whoever hold the prior to record date will be entitled for dividend payment. On record date, a firm makes a list from its stock transfer books of those shareholders who are eligible to receive the declared dividend (Aliahmed, 2011, p. 86-103).

Payment date: It is the date firm actually pays dividends to holders of record (Aliahmed, 2011, p. 86-103).

Dividend Payment Decision: Companies tend to change dividends steadily in response to a sustainable increase in earning. Cash dividends per year are more stable than earnings. Firms tend to pay higher dividends if the firm records higher earnings while lower dividends are paid out if the firm records lower earnings. Sometimes no dividends are paid even if the company makes profit or not. Hence, most firms tend to follow a stable dividend policy (Aliahmed, 2011, p. 86-103).

Alternative Dividend Policies;

Stock Dividend: The stock dividend is not common among the companies but some firms tend to distribute additional shares in the form of dividends to their shareholders rather than giving cash dividends (Aliahmed, 2011, p. 86-103).

Stock Split: When firms issue additional shares to their stockholders, no cash is exchanged for such additional shares. The only change occurs in the number of shareholdings and par value of shares. When a firm conducts a stock split, the stock price tends to decline as the number of shares increase. The number of shares is increased and par value is reduced proportionately (Aliahmed, 2011, p. 86-103).

Stock Repurchase: This is a common practice in developed and developing markets for a firm to buy back stock from its shareholders. It provides an effective substitute for dividends (Aliahmed, 2011, p. 86-103).

Repurchase as an Alternative to a Dividend: Firms with available cash on hand may put off paying dividends by repurchasing their own shares. This reduces the number of shares outstanding and increases the EPS of the remaining shares. Therefore, buying back shares results in a price appreciation (Aliahmed, 2011, p. 86-103).

Analysis of Companies’ dividend policies

The following table shows the ratio analysis of the companies to identify the dividend policies.

COMPANIES

|

AIRASIA BERHAD

|

MITRAJAYA HOLDINGS BERHAD

|

METAL RECLAMATION BHD

| ||||||

Ratios

|

2011

|

2010

|

2009

|

2011

|

2010

|

2009

|

2011

|

2010

|

2009

|

Dividend per share(Sen)=

|

2.8

|

0

|

0

|

4.71

|

9.40

|

0

|

0

|

0

|

0

|

Dividend yield (%) =

|

0.8

|

0

|

0

|

10

|

13.4

|

0

|

0

|

0

|

0

|

Earnings per share(RM)=

|

0.20

|

0.38

|

0.18

|

0.075

|

0.077

|

0.24

|

-0.01

|

-0.03

|

-0.03

|

Price earnings ratio=

|

18.3

|

7.1

|

7.7

|

6.3

|

9.1

|

1.0

|

-60

|

-30

|

-27

|

Dividend payout (%) =

|

14

|

0

|

0

|

62.8

|

122.1

|

0

|

0

|

0

|

0

|

Market price per share(RM)

|

3.65

|

2.70

|

1.38

|

0.47

|

0.70

|

0.25

|

0.60

|

0.90

|

0.82

|

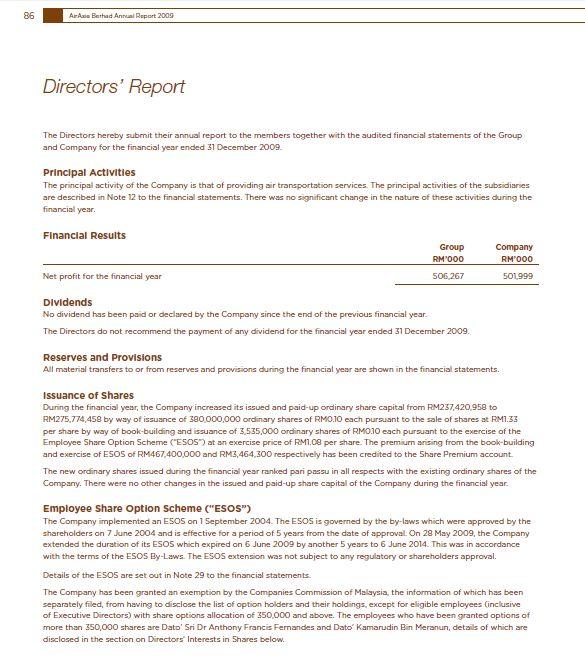

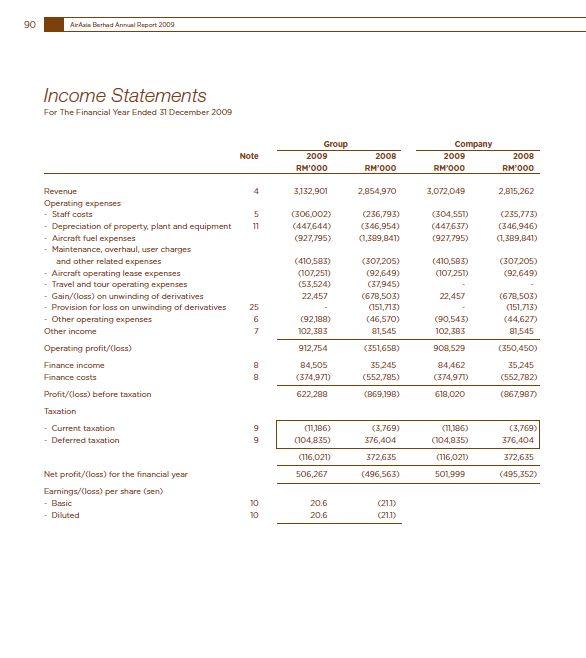

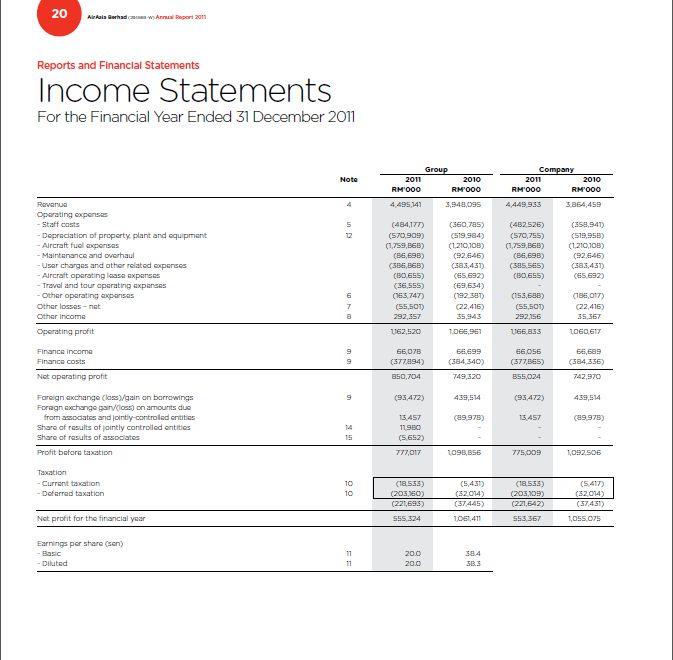

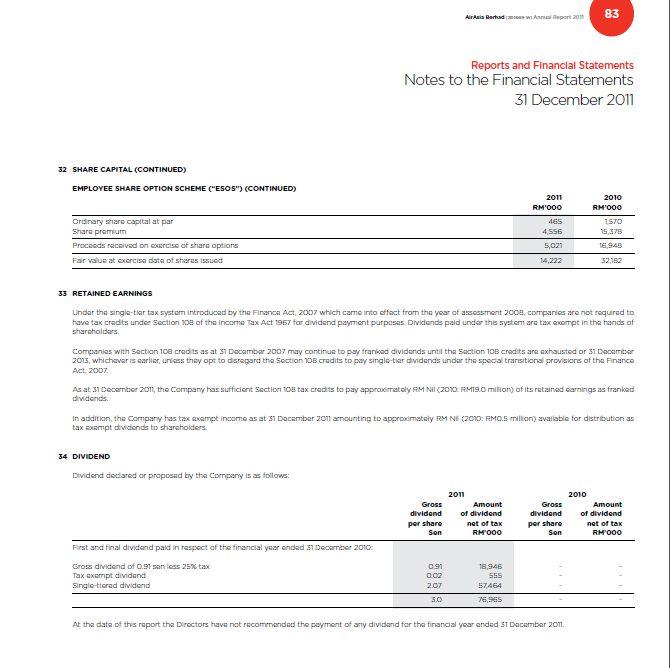

AirAsia Bhd:

The dividend per share is increased from 0 to 2.8 Sen in 2011. The dividend is not given to shareholders in 2010 and 2009. This means having a growing dividend per share can be a sign that the company's management believes that the growth can be sustained.

The dividend yield is increased from 0% to 0.8% in 2011. It indicates that 0.8% of cash flow is generated in 2011 for each Ringgit invested in the company by its shareholders which means that the performance of their investments is increased in 2011.

The earnings per share are increased from 0.18 RM to 0.38 RM from 2009 to 2010. However, it decreased from 0.38 RM to 0.20 RM in 2011. This means that the earning per ordinary share is decreasing. The available profit for distribution and expansion is decreasing which is not good for the ordinary shareholders because they are the risk takers.

Although the price earnings ratio is decreased to 7.1 in2010 it is increased from 7.7 to 18.3 from 2009 to 2011. This means that investors are expecting higher earnings growth of shares in the future.

The dividend payout ratio is increased from 0% to 14% from 2009 to 2011. The dividend payout ratio is 0% in 2009 and in 2010, which means that they retained 100% profit for further expansion of the company. In 2011, 14% profit is distributed as dividend which means 86% of the profit is used for further expansion.

The market price per share of 1.38 RM in 2009 is increased to 3.65 RM in 2011 and it shows a continuous increasing trend. This means that the shareholders share value is increasing and the shareholders can get more capital gain.

The table shows a signal effect of increasing the market share price per share due to paying dividend in 2011. The par value of the shares is 0.1 RM but in 2011, the market share price is 3.65 RM. Since the payout is 14% in 2011, the investors who need continuous dividend income will retain their shares to get future earnings and to get tax advantage. However, investors who need capital gain will sell the shares because it shows clientele effect.

The ratios show that the AirAsia Bhd is paying a dividend at irregular interval. They do not pay dividend every year in order to expand their business in future. In 2009 and 2010 they did not pay any dividend but in 2011, they paid a special dividend to its shareholders to maintain the shareholders interest. The other dividend policies include Employee Share Option Scheme. Instead of paying dividend in 2009 and 2010, the existing shareholders are offered bonus share by the company by crediting to the Share Premium account. Therefore, the share capital is increased in each year.

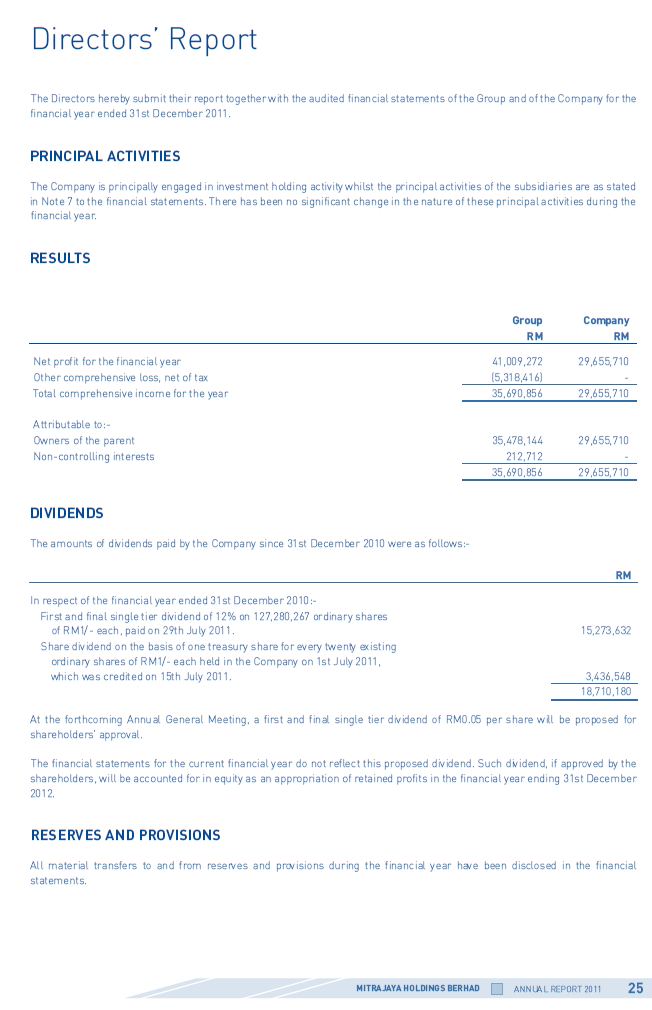

Mitrajaya Holdings Bhd

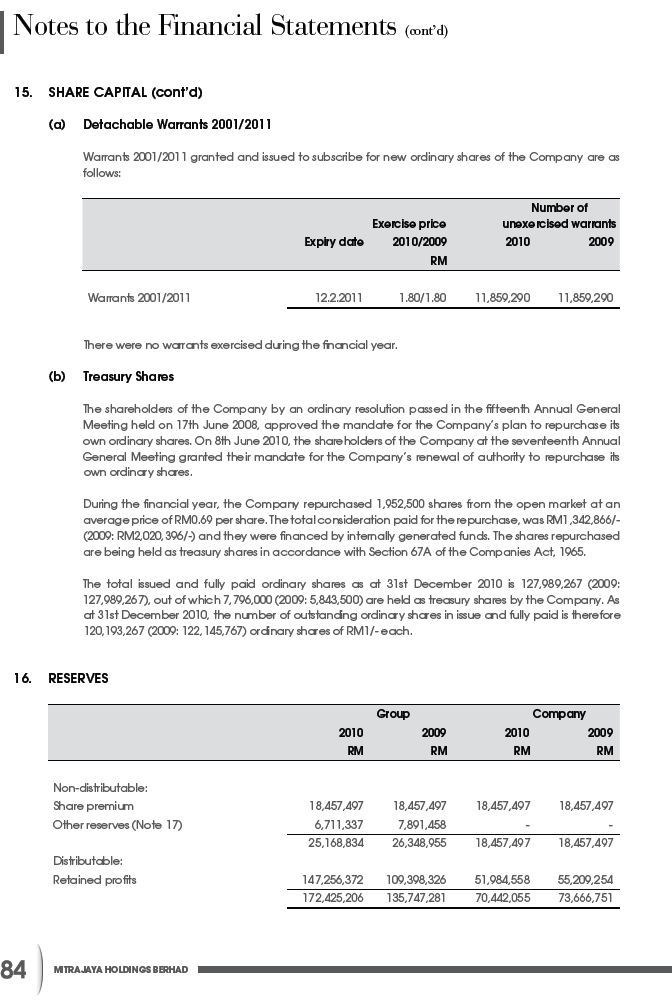

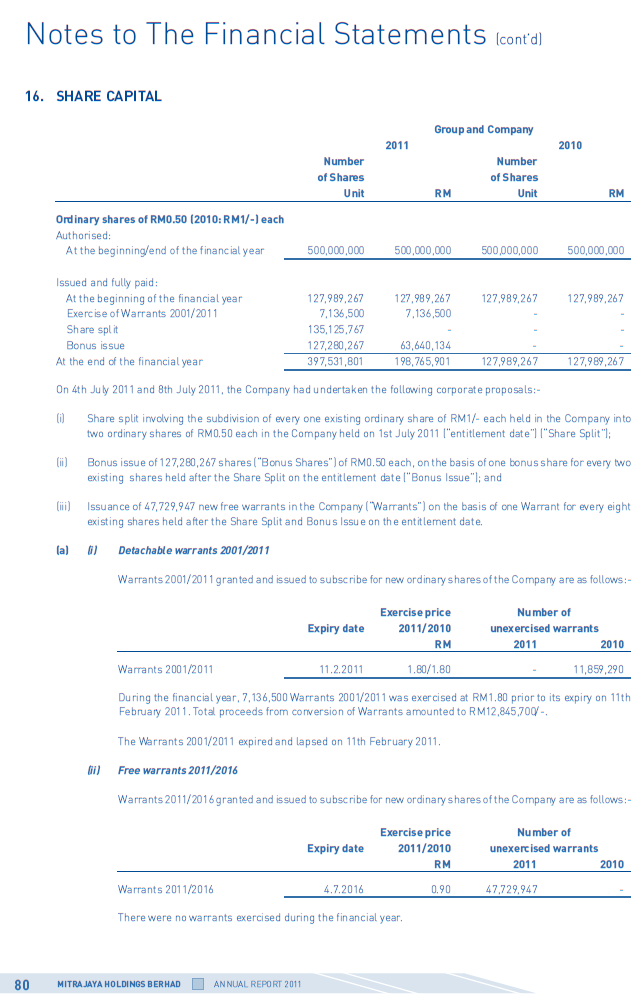

No dividend is paid in 2009 but in 2010 the dividend per share was 9.4 Sen and in 2011, it decreased to 4. 71 Sen. The dividends per share are decreased due to increase in number of ordinary shares in 2011.

The dividend yield is increased from 0% to 10% in 2011 but the dividend yield in 2010 is 13.4%. It indicates that 10% of cash flow is generated in 2011 for each Ringgit invested in the company by its shareholders which means that the performance of their investments is increased in 2011.

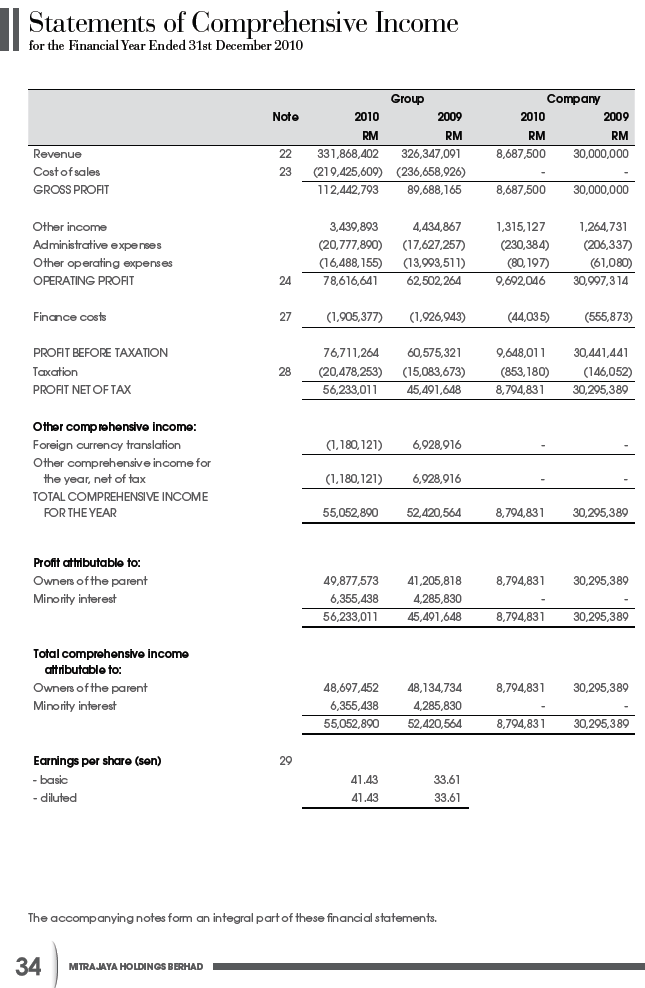

The earnings per share are decreased from 0.24 RM to 0.075 RM from 2009 to 2011. In 2010 the earning per share is 0.077 RM. This means that the earning per ordinary share is decreasing. The available profit for distribution and expansion is decreasing which is not good for the ordinary shareholders because they are the risk takers.

Although the price earnings ratio is increased to 9.1 in 2010, it is increased from 1.0 to 6.3 from 2009 to 2011. This means that investors are expecting higher earnings growth of shares in the future.

The dividend payout ratio is increased from 0% to 62.8% from 2009 to 2011. The dividend payout ratio in 2010 is 122.1%, which means that they are distributing more profit in 2010 and 2011. However, in 2009 they retained 100% profit for expansion.

The market price per share of 0.25 RM in 2009 is increased to 0.47 RM in 2011 but it increased to 0.70 RM in 2010. It shows fluctuating share price which indicates uncertainty of future share value.

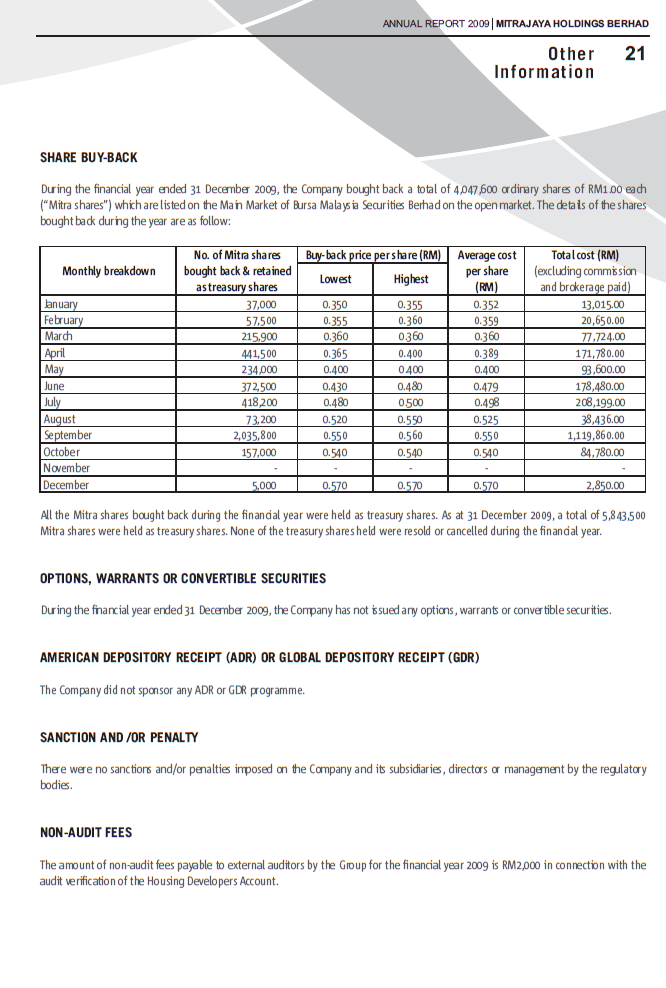

They are paying varying amount of dividend in 2011 and 2010. They have high payout ratio in theses two years and do not pay any dividend in 2009. During each year the company bought back ordinary shares. Although, the group has other dividend policies like bonus issue and share split, the company does not have these types of dividend policies.

This company has signal effect on shares because it shows 122.1% of dividend payout in 2010. As a result of this the market share price increased to 0.70 RM in 2010 and it decreased to 0.47 RM in 2011 due to decrease in dividend payout. This means that there can be clientele effect. The shareholders will sell the shares if they do not get more dividends.

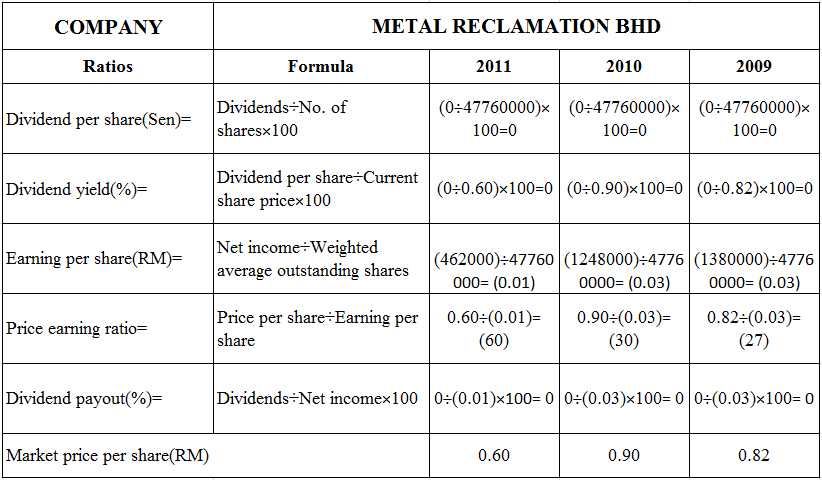

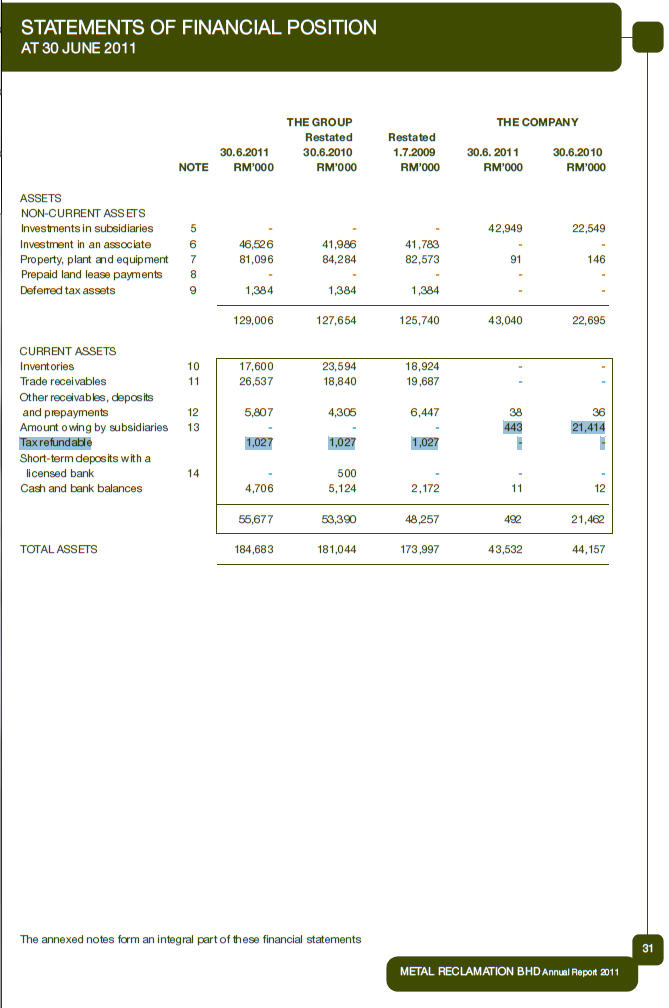

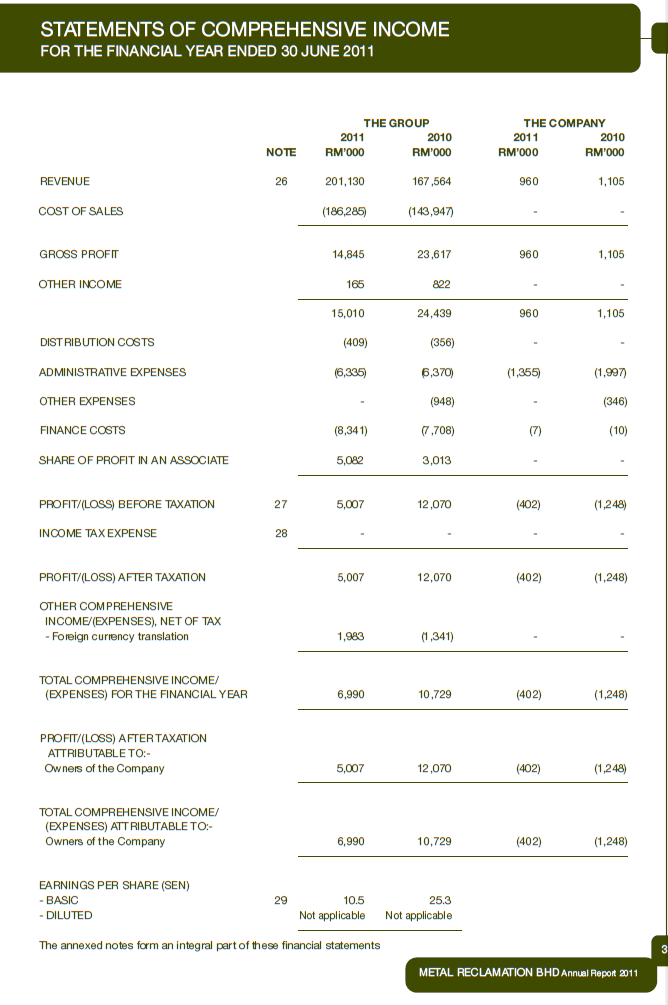

Metal Reclamation Bhd

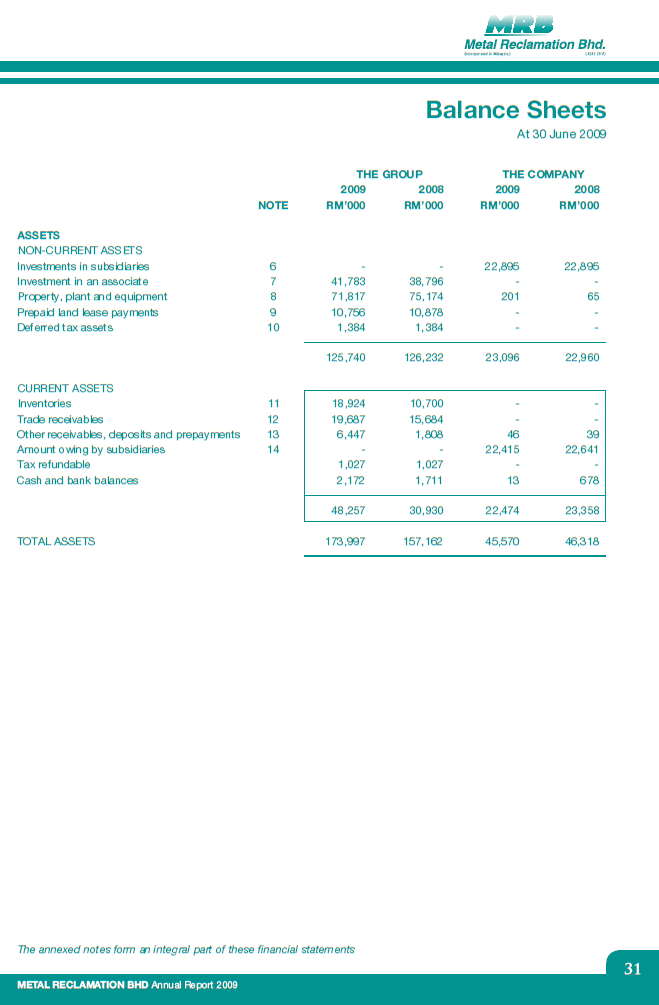

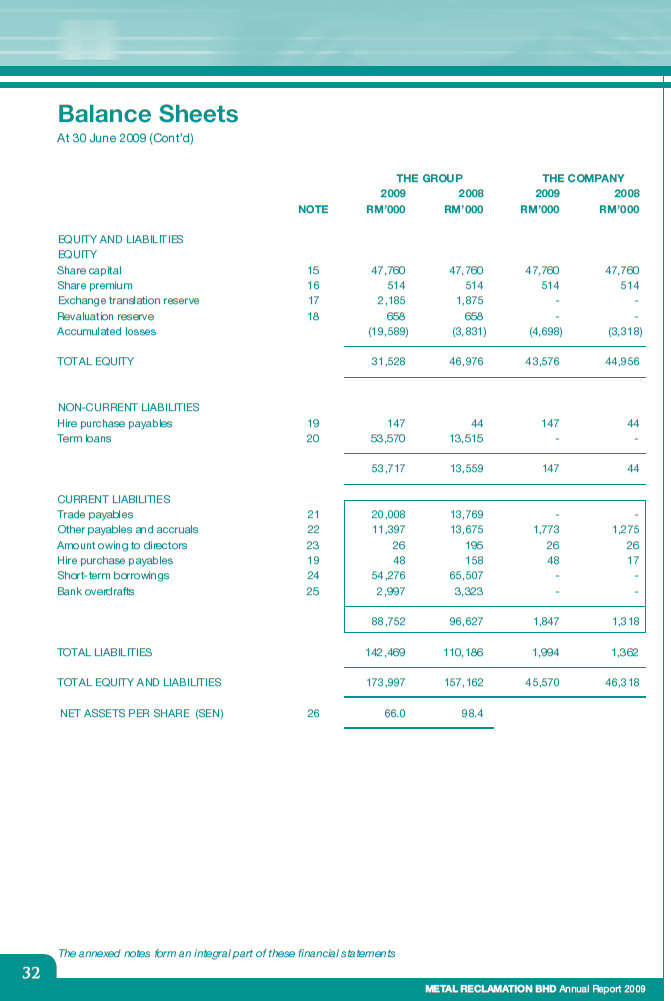

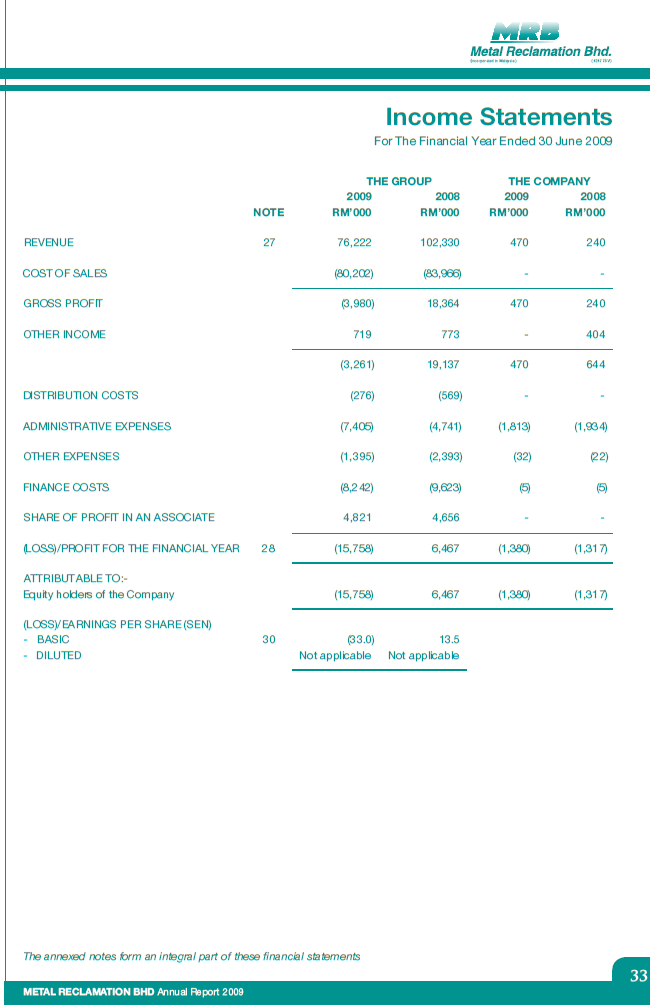

The table shows, the dividend per share is 0 in the three years hence the dividend yield percentage is 0. This is because they are making losses in the three years. Therefore, the earning per share is negative in theses years. The price earnings per share are negative in these periods. Since the company is making loss, the dividend payout is 0% and do not have any retain earnings for future expansions of the company. The market per share is decreased from 0.82 RM to 0.60 RM from 2009 to 2011 but it increased to 0.90 RM in 2010.

As a result of making losses and not paying dividend, it shows a signal effect of decreasing the market share price of the company cautiously. The par value of the share is 1 RM but the market share price decreased to 0.60 RM in 2011. Since it shows the payout ratio is 0 and there can be clientele effect on shares because investors need not to maintain their shares in a loss making company. However, there is no sale or purchase of shares during the periods.

In a nutshell, the company’s dividend policy is not to pay any dividend because of making losses in these three years. Meantime, they do not have any other dividend policy and the share premium is not distributable by way of dividends during these periods.

Comparison of Companies’ dividend policies

The highest dividend per share is in Mitrajaya Holdings Bhd and the least dividend per share is in Metal Reclamation Bhd. Meantime, the dividend per share of AirAsia Bhd is increased in 2011. The least dividend yield percentage is in Metal Reclamation Bhd and the highest dividend yield is in Mitrajaya Holdings Bhd. The highest earning per share is in AirAsia Bhd and the least earning per share is in Metal Reclamation Bhd. The highest price earnings ratio is in AirAsia Bhd and the least is in Metal Reclamation Bhd. The highest dividend payout ratio is in Mitrajaya Holdings Bhd and the least is in Metal Reclamation Bhd. The highest market share price is in AirAsia Bhd and has an increasing trend. The least market share price is in Mitrajaya Holdings Bhd and it shows a decreasing trend. Also, the market share price of Metal Reclamation Bhd is decreasing.

The Miller-Modigliani Hypothesis says paying dividends do not affect value of firm. If a firm's investment policy and hence cash flows don't change, the value of the firm cannot change with dividend policy. If we ignore personal taxes, investors have to be indifferent to receiving either dividends or capital gains (Aliahmed, 2011, p. 86-103).

Underlying Assumptions are; if there are no tax differences between dividends and capital gains. If companies pay too much in cash, they can issue new stock, with no flotation costs or signaling consequences, to replace this cash. If companies pay too little in dividends, they do not use the excess cash for bad projects or acquisitions (Aliahmed, 2011, p. 86-103).

Dividends are taxed more heavily than capital gains. A stockholder will therefore prefer to receive capital gains over dividends. Examining ex-dividend dates should provide us with some evidence on whether dividends are perfect substitutes for capital gains (Aliahmed, 2011, p. 86-103).

Bird-in-the hand theory says dividends now are more certain than capital gains later. Hence dividends are more valuable than capital gains. However, the appropriate comparison should be between dividends today and price appreciation today. (The stock price drops on the ex-dividend day) (Aliahmed, 2011, p. 86-103).

If the firm has excess cash on its hands this year, no investment projects this year and can to give the money back to stockholders. Meantime, firm can repurchase stock and the firm has to consider future financing needs. The firm also needs to consider the cost of issuing new stock (Aliahmed, 2011, p. 86-103).

Management Beliefs about Dividend Policy: A firm’s dividend payout ratio affects its stock price. Dividend payments operate as a signal to financial markets. Dividend announcements provide information to financial markets. Investors think that dividends are safer than retained earnings. Investors are not indifferent between dividends and price appreciation. Stockholders are attracted to firms that have dividend policies that they like (Aliahmed, 2011, p. 86-103).

In the case of dividends and stock buybacks, firms change the value of the assets (by paying out cash) and the number of shares (in the case of buybacks). However, there are other factors that influence dividend policy of the firm. The debt contracts contain provisions that restrict dividend policy. Typically, common dividends cannot be paid if the company has passed its preferred dividends. Dividend payments cannot exceed the balance sheet value for retained earnings. Dividend must be paid with cash and cash shortage may arise. If the management is concerned about control, then it may be reluctant to sell new common stock (Aliahmed, 2011, p. 86-103).

It is understood that for Metal Reclamation Bhd, the major factors that influence their dividend policy are their losses and low cash flows in these years. Whereas the major factor that influenced the dividend policies of Mitrajaya Holdings Bhd and AirAsia Bhd is their future expansion plans because they retained more profit in these years.

The table shows that Metal Reclamation Bhd is following Miller-Modigliani theory in these three years. They do not pay any dividend to the shareholders during these periods. It shows a fluctuating effect of market share price in these years. Therefore, Miller’s argument is true in this case.

The table shows that Mitrajaya Holdings Bhd is following Miller-Modigliani theory in 2009 where as they are following Bird-in-the hand theory in 2010 and 2011. In this case it shows an increase in market share price in 2010 when high dividend is paid. Also, the market share price is decreased in 2011 due to decrease in dividend payment. So, it is understood that paying dividend affects the firm’s value. Therefore, Bird-in-the hand theory is correct and relevant in this situation.

The table also shows that AirAsia Bhd is following Miller-Modigliani theory in 2009 and 2010. At a same time, they are using Bird-in-the hand theory in 2011. In this case, the market share prices in 2009 and 2010 are increased even no dividend is paid in theses periods. The market share price is also increased in 2011 when dividend is paid by the company. So, it is understood that paying dividend does not affect the firm’s value and paying dividend also affect the firm’s value too. Therefore, both theories are correct and relevant.

Conclusion

The analysis of dividend policies of the three companies has identified the different dividend policies in each company. AirAsia Bhd is paying a dividend at irregular interval and has other dividend policies of Employee Share Option Scheme. Mitrajaya Holdings Bhd is paying varying amount of dividend at irregular interval and has share buyback policy. Metal Reclamation Bhd policy is not to pay dividend and they do not have other dividend policies compared to others. Meantime, all these three companies have different signal effect on their shares.

Since AirAsia Bhd and Mitrajaya Holdings Bhd have excess cash and few good projects, returning money to stockholders (dividends or stock repurchases) is a good decision but it is not advisable to Mitrajaya Holdings Bhd to have high payout because this will affect their share price and liquidity problems will occur. Since Metal Reclamation Bhd does not have excess cash and have several good projects, returning money to stockholders is bad.

The Miller-Modigliani and Bird-in-the hand theories are correct and applicable depending on the situations. Therefore, paying some amount of dividend is much better than not paying any dividend to the shareholders.

Appendix 1: Workings for Metal Reclamation Company

Appendix 2: Workings for AirAsia Company

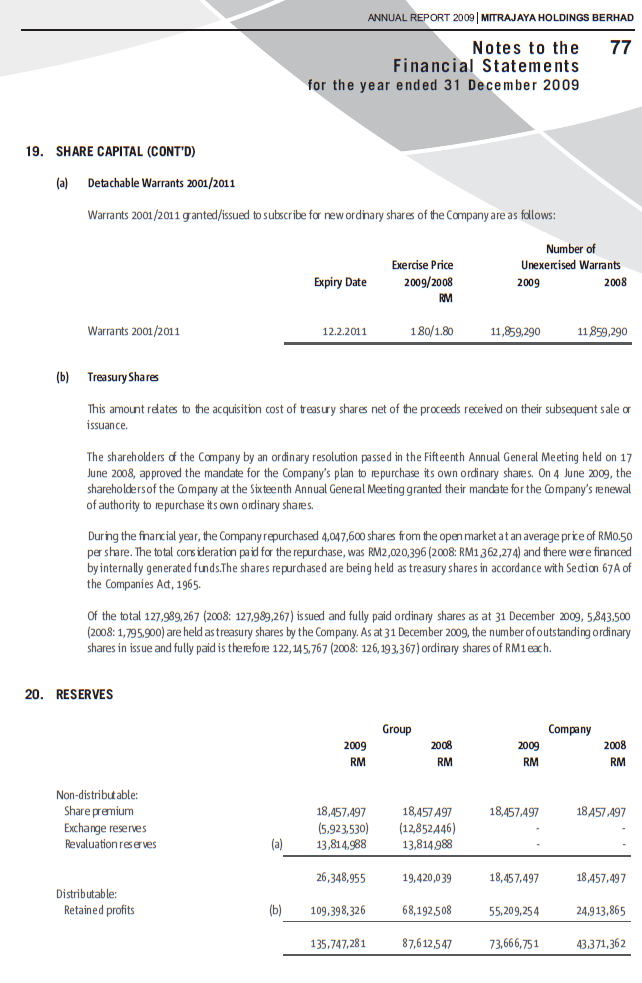

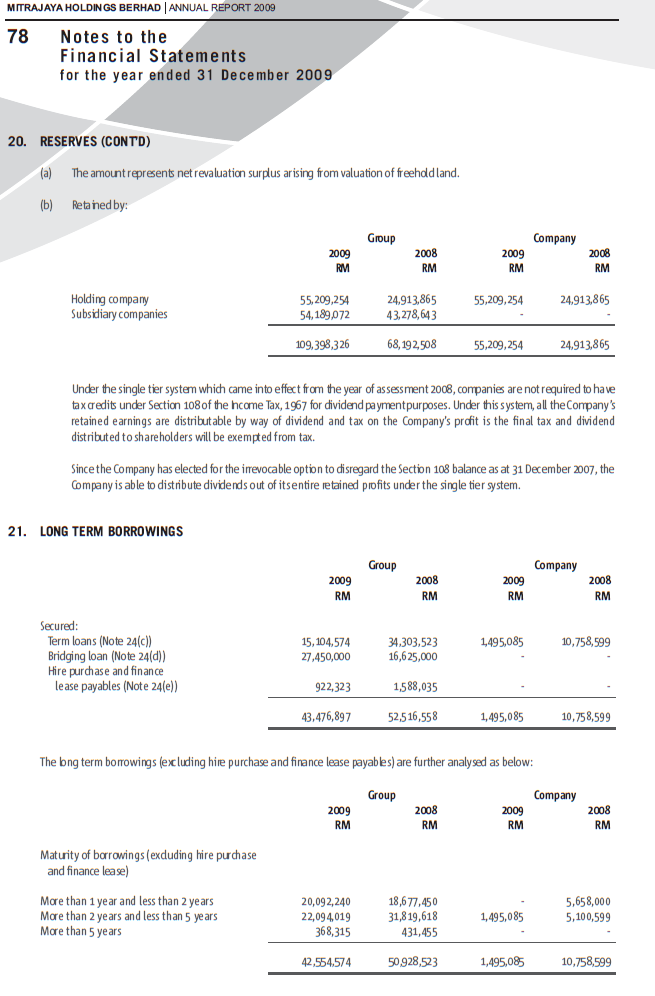

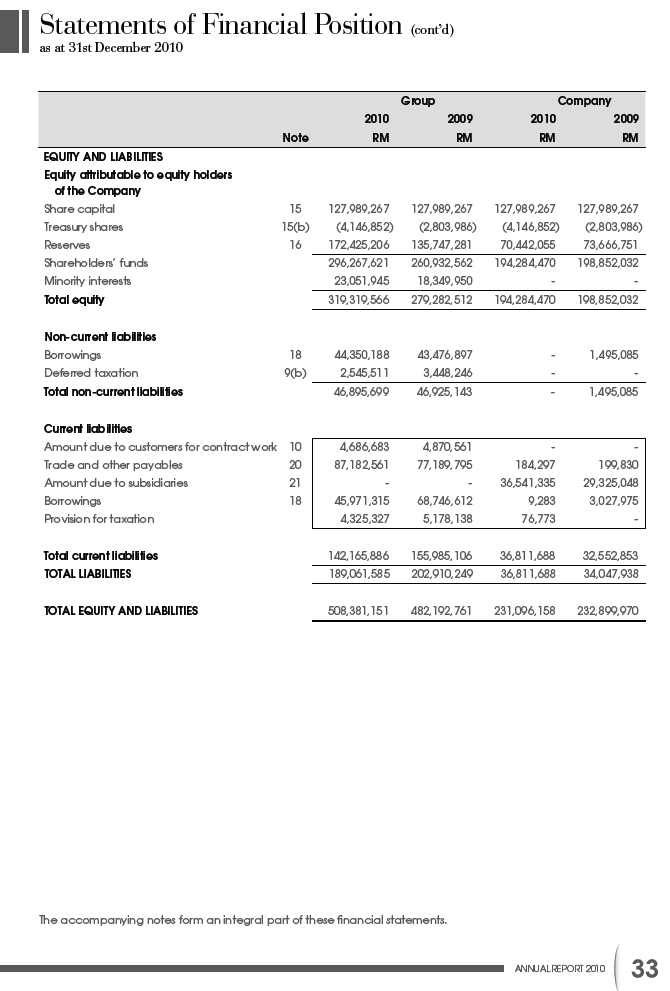

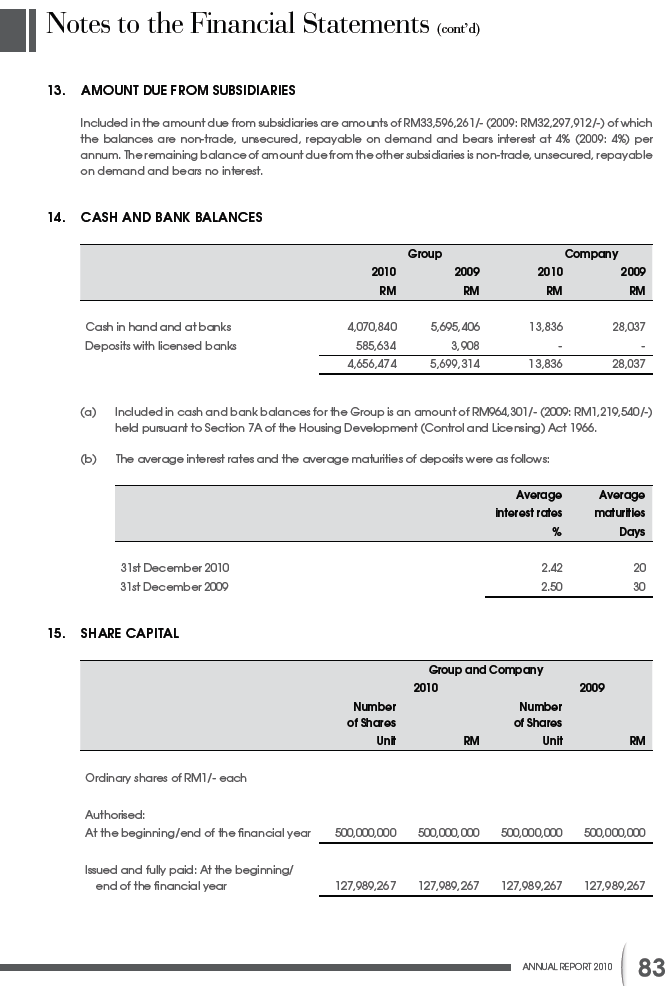

Appendix 3: Workings for Mitrajaya Holdings Company

Appendix 4: Annual accounts of Metal Reclamation Company

Appendix 5: Annual accounts of AirAsia Company

Appendix 6: Annual accounts of Mitrajaya Holdings Company

References

AirAsia: Corporate profile. (2012). Retrieved October 16, 2012, from http://www.airasia.com/cn/en/corporate/corporateprofile.page?

Aliahmed., H., J. (2011, p. 86-103). FINANCIAL MANAGEMENT II, Topic 4: Dividend Policy. Malaysia: Meteor Doc. Sdn. Bhd.

Annual Report. (2011). AirAsia Berhad. Retrieved October 16, 2012, from http://www.airasia.com/iwov-resources/my/common/pdf/AirAsia/IR/AA-Financials-2011.pdf

Annual Report. (2010). AirAsia Berhad. Retrieved October 16, 2012, from http://www.airasia.com/iwov-resources/my/common/pdf/AirAsia/IR/AirAsia_AR10.pdf

Annual Report. (2009). AirAsia Berhad. Retrieved October 16, 2012, from http://www.airasia.com/iwov-resources/my/common/pdf/AirAsia/IR/AirAsia_AR09.pdf

Annual Report. (2011). Metal Reclamation Berhad. Retrieved October 16, 2012, from http://announcements.bursamalaysia.com/EDMS%5Csubweb.nsf/LsvAllByID/CE9AC5F77DA078F94825795200184075?OpenDocument

Annual Report. (2010). Metal Reclamation Berhad. Retrieved October 16, 2012, from http://announcements.bursamalaysia.com/EDMS/subweb.nsf/all/CF11CF3B26B7A2E74825793700157F64/$File/Metal%20R_Audited%20Accounts%20FY2011.pdf

Annual Report. (2009). Metal Reclamation Berhad. Retrieved October 16, 2012, from http://www.google.mv/url?sa=t&rct=j&q=METAL+RECLAMATION+BERHAD+annual+report+2009+pdf&source=web&cd=2&cad=rja&ved=0CCAQFjAB&url=http%3A%2F%2Fwww.researchandmarkets.com%2Freports%2F1427349%2Fmetal_reclamation_bhd_2009_annual_report.pdf&ei=RXKKUIDFJ4SQiAfSlYGQBw&usg=AFQjCNEX3mLrGIZ9KTosVcIb0kDZQJlbuA

Annual Report. (2011). Mitrajaya Holdings Berhad. Retrieved October 15, 2012, from http://announcements.bursamalaysia.com/EDMS/subweb.nsf/7f04516f8098680348256c6f0017a6bf/a21678f0df32c00b48257a0000326db5/$FILE/MITRA-AnnualReport2011%20%281.2MB%29.pdf

Annual Report. (2010). Mitrajaya Holdings Berhad. Retrieved October 15, 2012, from http://announcements.bursamalaysia.com/EDMS/subweb.nsf/7f04516f8098680348256c6f0017a6bf/9ac3804f935d91c3482578920029dbed/$FILE/MITRA-AnnualReport2010%20%282.5MB%29.pdf

Annual Report. (2009). Mitrajaya Holdings Berhad. Retrieved October 15, 2012, from http://announcements.bursamalaysia.com/EDMS/subweb.nsf/7f04516f8098680348256c6f0017a6bf/3f0722bd9ca53ac94825772600267414/$FILE/MITRA-AnnualReport2009%20%281.5MB%29.pdf

Metal Reclamation Bhd: About us. (2012). Retrieved October 16, 2012, from http://www.metalreclamationbhd.com/about.html

Mitrajaya: Our business portfolio. (2012). Retrieved October 16, 2012, from http://www.mitrajaya.com.my/bizportfolio.html

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.