Open University Malaysia

Faculty of Business and Management

BBAP 2103

Management Accounting

Name: Adam Khaleel

Lecturers: Mohamed Azeem Haroon

Learning Centre: Villa College

Trimester: May 2012

Table of Contents

Executive Summary

This assignment will focus on the cost concepts and different types of costs incurred in the firms. The cost classification based on behaviour, function and period will be discussed. In addition to this, Toll Brothers, a construction organization which follows job costing system and Pacific Electronics, an electronics items manufacturing organization which follows process costing system are selected to describe the job and the process of these two firms. A detailed calculation and discussion on how they calculate the total cost per unit in each system will be given. For the process costing firm two different methods will be used to calculate the cost per unit and for the job costing firm the total cost for the individual job will be calculated. Finally, a discussion will be given on how these two systems differ from each other.

Introduction

In every business organization there are different types of costs for the firm. Jamaludin et al. (2011, p.9) has found that the Cost is any resources that have to be given up in order to obtain goods or services. Resource is equivalent to assets because the assets that are not used in this period can be used in the future which is called unexpired assets. This resource will become an expense once they are used up.

Jamaludin et al. (2011, p.61) has found that the job order costing system prepares separate records of cost information for each product quantity which is known as a job that passes through the production process such as construction business. Jamaludin et al. (2011, p.87) has found that the Process costing is suitable for a product that uses constant resources or the same resources used for each product unit such as electronics firm. It includes sequential processing and parallel processing.

Jamaludin et al. (2011, p.12-16) has found there are different cost incurred in the company which includes fixed cost, variable cost and mixed cost. Fixed cost includes rent, insurance, accountancy cost etc. variable cost includes electricity, material, labour, delivery cost etc. Mixed cost includes electricity and telephone bills. Direct material, direct labour, overheads, administrative and sales expenses are also the costs incurred in the firms.

The main purpose of this assignment is to develop the skills in applying product costing in different organizations. This assignment mainly talks about firstly, the description on the classification of costs. Secondly, the discussion will be given on the total cost per unit calculation for Toll Brothers which uses job costing system. Thirdly, the discussion on how total cost per unit is calculated in process costing system of Pacific Electronics will be given. Finally, a conclusion of the assignment will be given.

Costs Classification

Jamaludin et al. (2011, p.12-21) has found that the Cost classification according to behaviour is the cost that is observed through its behaviour on production of units which includes fixed, variable and mixed costs. Fixed cost is the cost that does not vary with production level such as rent. Variable cost is the cost that varies according to changes in production units such as raw material. Mixed cost is the cost that contains components of fixed cost and variable cost

Jamaludin et al. (2011, p.12-21) has found that the Cost classification according to business function is the cost that is classified according to the operations that is carried out by a business. It includes manufacturing operation function and non-manufacturing operation function. A manufacturing operation is an operation that processes raw materials to finished goods. A non-manufacturing operation includes commercial operation that carries out the activity of buying and selling finished goods and service operation that provides a service to others.

Jamaludin et al. (2011, p.12-21) has found that the Manufacturing cost is the same as production cost which comprises of the costs of direct materials, direct labour and factory overhead. Direct materials cost is the cost of the raw materials used directly in making the product and it can be traced out. Direct labour cost is made up of the salaries and wages given to employees involved directly in making the finished goods. An overhead cost includes all the cost that is put into production other than direct raw materials and direct labour.

Jamaludin et al. (2011, p.12-21) has found that the Manufacturing cost includes prime cost and conversion costs. Prime cost is the main cost of direct materials and direct labour that are used in making the finished goods. Conversion cost includes direct labour and overhead. Non-manufacturing cost is the cost of traded goods for a commercial firm such as marketing cost and administrative cost.

Jamaludin et al. (2011, p.12-21) has found that the Cost classification according to period is the cost which is incurred in a specific time period such as fixed cost which includes product cost and period cost. Product cost is the cost that is provided directly to the product such as raw material. Period cost is the cost that is charged as an expense in the period it occurs. Administrative and sales expenses can be considered as period costs.

Job costing system

Toll Brothers build homes and communities. Since 1967, they have been building communities in picturesque settings where luxury meets convenience and where neighbors become lifelong friends. Each Toll Brothers home offers a combination of quality materials and superior design where every detail is meticulously crafted. Toll Brothers is the nation's premier builder of luxury homes and is a public limited company whose stock is listed on the New York Stock Exchange. (Pacific Electronics, n.d.).

Toll Brothers is going to frame the interior and exterior walls of the Simpson family’s new 2,500-square-foot custom home and the Job number for Simpson home is 2719. The following picture shows how this particular job will be completed. (Chapter 2: Job Order Costing, n.d.).

The picture shows the three types of costs that will be incurred in this lob. Examples of direct materials used in building a home include concrete, piping, lumber, drywall, fixtures etc. Direct labor used in building a home includes the work of pouring the foundation, framing the home, and installing the plumbing. Manufacturing overhead required to build home include the costs of site supervision, construction insurance, depreciation. (Chapter 2: Job Order Costing, n.d.).

The following documents are the material requisition form, the job cost sheet and direct labour time ticket for the job no.2719 for the date of 08th November 2010. (Chapter 2: Job Order Costing, n.d.).

Assume Toll Brothers estimates the total manufacturing overhead cost for the upcoming year to be $750,000 and total direct labor hours to be 10,000. (Chapter 2: Job Order Costing, n.d.).

Jamaludin et al. (2011, p.67-68) has found that the Indirect manufacturing overhead costs must be assigned to specific jobs using a secondary measure called an allocation base. Therefore the overhead absorption rate = estimated budgeted overheads ÷ estimated total budgeted basis. Overhead Applied to an Individual Job = Predetermined Overhead Rate × Actual Value of the Allocation Base for Each Job.

OAR = 750000 / 10000

OAR = $75

Manufacturing overheads for the Job no. 2719 = (300×75) = $22500

The overhead absorption may be over absorbed or under absorbed because the OAR is based on estimation. If the overhead absorption is greater than actual overheads, then it is an over absorption and vice versa.

Cost summary for the Job number 2719

|

$

|

Direct Material

|

30000

|

Direct Labour (300×25)

|

7500

|

Manufacturing overheads (300×75)

|

22500

|

Total Cost

|

60000

|

The job cost sheet shows the total cost of $60000 which is for the Job no. 2179 only because this could be the only Job they had at that time. Therefore the total cost per unit = total cost ÷ total number of finished units. The total cost per unit = 60000÷1 = $60000.

Process Costing System

Pacific Electronics is a leading manufacturer of quality OEM and aftermarket electronic products and components for industry, retailers and consumers. They produce quality electronic components and products for a large and diverse customer base- motors, fans, transformers, connectors, electronic communication devices and much more. (Pacific Electronics, n.d.).

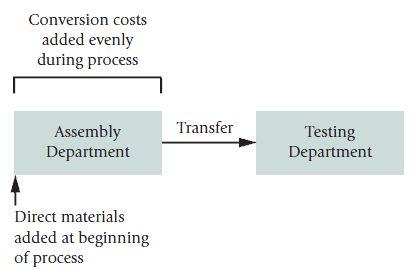

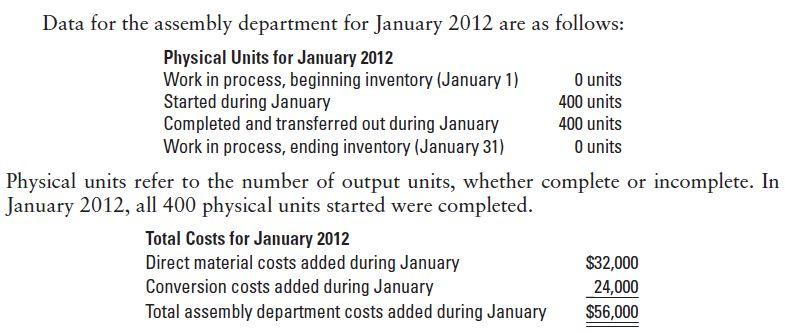

Suppose that Pacific Electronics manufactures a variety of cell phone models. These models are assembled in the assembly department and transferred to the testing department. All units of SG-40 are identical. The process-costing system for SG-40 in the assembly department includes direct materials and conversion costs. Direct materials are added at the beginning of the assembly process. Conversion costs are added evenly during assembly. The following diagram shows

the details. (Process Costing, n.d.).

the details. (Process Costing, n.d.).

(Process Costing, n.d.) Case 3 has found the above data.

First In First Out Method(FIFO)

| ||||||||||||||

Statement of equivalent units

| ||||||||||||||

Entries

|

Units

|

Degree of completion: Direct materials (100%)

|

Degree of completion: Conversion costs (50%)

| |||||||||||

Opening inventory of WIP

|

225

|

0

|

90

| |||||||||||

Completed units during the period

|

175

|

175

|

175

| |||||||||||

Total units completed

|

400

|

175

|

265

| |||||||||||

Closing inventory of WIP

|

100

|

100

|

50

| |||||||||||

Total units

|

500

|

275

|

315

| |||||||||||

Statement of cost per equivalent units

| ||||||||||||||

Direct materials

|

Conversion costs

| |||||||||||||

Cost per unit =

|

(19800/275) = $72

|

(16380/315) = $52

| ||||||||||||

Statement of evaluation

| ||||||||||||||

Entries

|

Equivalent unit: Direct materials

|

Equivalent unit: Conversion costs

|

Total

| |||||||||||

Opening inventory of WIP

|

(72×0)+18000 = 18000

|

(52×90)+8100 = 12780

|

30780

| |||||||||||

Completed units during the period

|

(72×175) = 12600

|

(52×175) = 9100

|

21700

| |||||||||||

Closing inventory of WIP

|

(72×100) = 7200

|

(52×50) = 2600

|

9800

| |||||||||||

62280

| ||||||||||||||

Process Account

| ||||||||||||||

Units

|

$

|

Units

|

$

| |||||||||||

Opening stock: WIP; Material

|

225

|

18000

|

Output process in WIP

|

225

|

30780

| |||||||||

Conversion costs

|

8100

|

Output from process

|

175

|

21700

| ||||||||||

Process Input; Material

|

275

|

19800

|

Closing stock: WIP

|

100

|

9800

| |||||||||

Conversion costs

|

16380

| |||||||||||||

500

|

62280

|

500

|

62280

| |||||||||||

Weighted average Method(AVCO)

| |||||||||||||

Statement of equivalent units

| |||||||||||||

Entries

|

Units

|

Degree of completion: Direct materials (100%)

|

Degree of completion: Conversion costs (50%)

| ||||||||||

Opening inventory of WIP

|

225

|

225

|

225

| ||||||||||

Completed units during the period

|

175

|

175

|

175

| ||||||||||

Total units completed

|

400

|

400

|

400

| ||||||||||

Closing inventory of WIP

|

100

|

100

|

50

| ||||||||||

Total units

|

500

|

500

|

450

| ||||||||||

Statement of cost per equivalent units

| |||||||||||||

Direct materials

|

Conversion costs

| ||||||||||||

Opening stock: WIP

|

18000

|

8100

| |||||||||||

Processed cost

|

19800

|

16380

| |||||||||||

Total cost

|

37800

|

24480

| |||||||||||

Cost per unit =

|

(37800/500) = $75.60

|

(24480/450) = $54.40

| |||||||||||

Statement of evaluation

| |||||||||||||

Entries

|

Equivalent unit: Direct materials

|

Equivalent unit: Conversion costs

|

Total

| ||||||||||

Completed units during the period

|

(400×75.60) = 30240

|

(400×54.40) = 21760

|

52000

| ||||||||||

Closing inventory of WIP

|

(100×75.60) = 7560

|

(50×54.40) = 2720

|

10280

| ||||||||||

62280

| |||||||||||||

Process Account

| |||||||||||||

Units

|

$

|

Units

|

$

| ||||||||||

Opening stock: WIP; Material

|

225

|

18000

|

Output from process

|

400

|

52000

| ||||||||

Conversion costs

|

8100

|

Closing stock: WIP

|

100

|

10280

| |||||||||

Process Input; Material

|

275

|

19800

| |||||||||||

Conversion costs

|

16380

| ||||||||||||

500

|

62280

|

500

|

62280

| ||||||||||

Since there is no opening and closing stock of work in progress and the input are 400 units at a cost of $56000 on 1st January, 2012. (Process Costing, n.d.). Case 1.Assume the output is 340 units and the normal loss is 12.5% of the inputs. Then the treatment losses are shown below;

Normal loss

|

(400×12.5/100) = 50 units

|

Abnormal loss

|

(350-340) = 10 units

|

Cost per unit

|

(56000/350) = $160

| ||||||||||||

Process Account

| |||||||||||||||||

Units

|

$

|

Units

|

$

| ||||||||||||||

Input

|

400

|

56000

|

Output

|

340

|

54400

| ||||||||||||

Normal loss

|

50

|

0

| |||||||||||||||

Abnormal loss

|

10

|

1600

| |||||||||||||||

400

|

56000

|

400

|

56000

| ||||||||||||||

Abnormal loss Account

| |||||||||||||||||

Units

|

$

|

Units

|

$

| ||||||||||||||

Process a/c

|

10

|

1600

|

Income statement

|

10

|

1600

| ||||||||||||

10

|

1600

|

10

|

1600

| ||||||||||||||

Conclusion

In conclusion, the costs are the expired resources and it can be classified according to the behavior, function and period. The total cost of the job in Toll Brothers is calculated by adding direct material and direct labour and the overhead which is apportioned by using predetermined overhead absorption rate for the individual job. The total cost per unit of process costing of Pacific electronics is calculated by using FIFO and AVCO methods. The main differences between job costing and process costing are how the costs are assigned and how the cost per unit is calculated in each system. In a job-costing system, individual jobs use different quantities of production resources and it would be wrong to cost each job at the same average production cost. However, the process costing is used to calculate an average production cost for all units produced.

References

Chapter 2: Job Order Costing. (n.d.). Assigning Manufacturing Costs to Jobs. Retrieved June 04, 2012, from http://highered.mcgraw-hill.com/sites/dl/free/0078110777/806287/chapter_02_job_order_costing.pdf

Jamaludin, N. A., Lode, N. A., Ahmad, J. H., Abidin, A. Z., Ali, A., Abd. Aziz, N. M., Mohamed, R. (2011). Management Accounting. Malaysia: Meteor Doc. Sdn. Bhd.

Pacific Electronics. (n.d.). Home. Retrieved June 03, 2012, from http://www.pacificelectronicscorp.com/page101.html

Process Costing. (n.d.). Case 1. Retrieved June 04, 2012, from http://ebooks.narotama.ac.id/files/Cost%20Accounting-A%20Managerial%20Emphasis%20%2814th%20Edition%29/Chapter%2017%20Process%20Costing.pdf

Process Costing. (n.d.). Case 3. Retrieved June 04, 2012, from http://ebooks.narotama.ac.id/files/Cost%20Accounting-A%20Managerial%20Emphasis%20%2814th%20Edition%29/Chapter%2017%20Process%20Costing.pdf

Tall Brothers. (n.d.). About Tall Brothers. Retrieved June 03, 2012, from http://www.tollbrothers.com/about

Apendix-1

Documents of Toll Brothers

Apendix-2

Documents of Pacific Electronics

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.